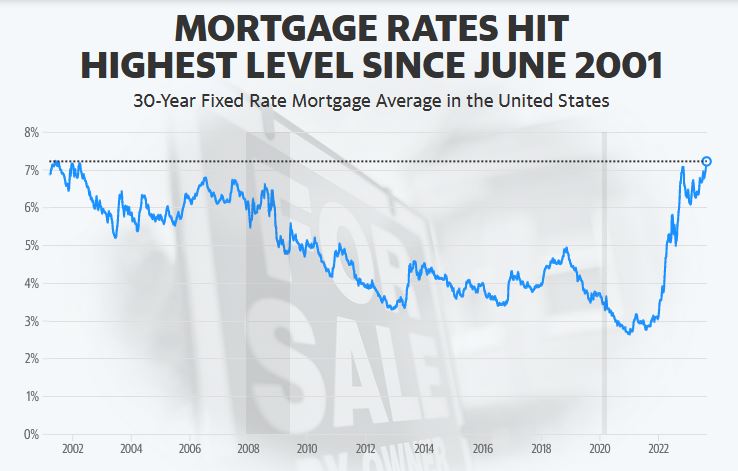

The average 30-year mortgage rate jumped to 7.23% this week, up from last week’s 7.09%, according to Freddie Mac on Thursday. That is the highest rate point since June 2001 when rates were at 7.24%.

Today’s rate environment is bruising first-time homebuyers who are facing many other struggles, including high prices and minimal inventory. The resulting unaffordability is also increasing the wealth gap between those who own and those who remain stuck on the sidelines.

Read more: What the Fed rate hike means for mortgage rates and loans

“It’s going to create a huge social divide,” Lawrence Yun, chief economist with the National Association of Realtors, told Yahoo Finance Live (video above) about mortgage rates. “Homeowners are smiling big, while the renters feel like their dream is out of reach, frustrated that other people are getting the housing wealth while they are left out paying higher rents each month.”

‘Shut out of the market’

Many buyers have thrown in the towel.

The volume of mortgage applications for a home purchase was the smallest in 28 years last week, according to an index from the Mortgage Bankers Association released Wednesday. The seasonally adjusted index dropped by 5% for the week ending Aug. 18 from the previous week, and was 30% percent lower than a year ago on an unadjusted basis.

“As rates have surged past 7% and homebuying costs have risen yet again, home purchase mortgage applications have eased, suggesting that at least some potential buyers have been shut out of the market,” Danielle Hale, Realtor.com’s chief economist, said.

Leave a comment